Source:

https://www.nritaxservice.in/blog/2025/06/19/foreign-retirement-funds-tax-implications-india/

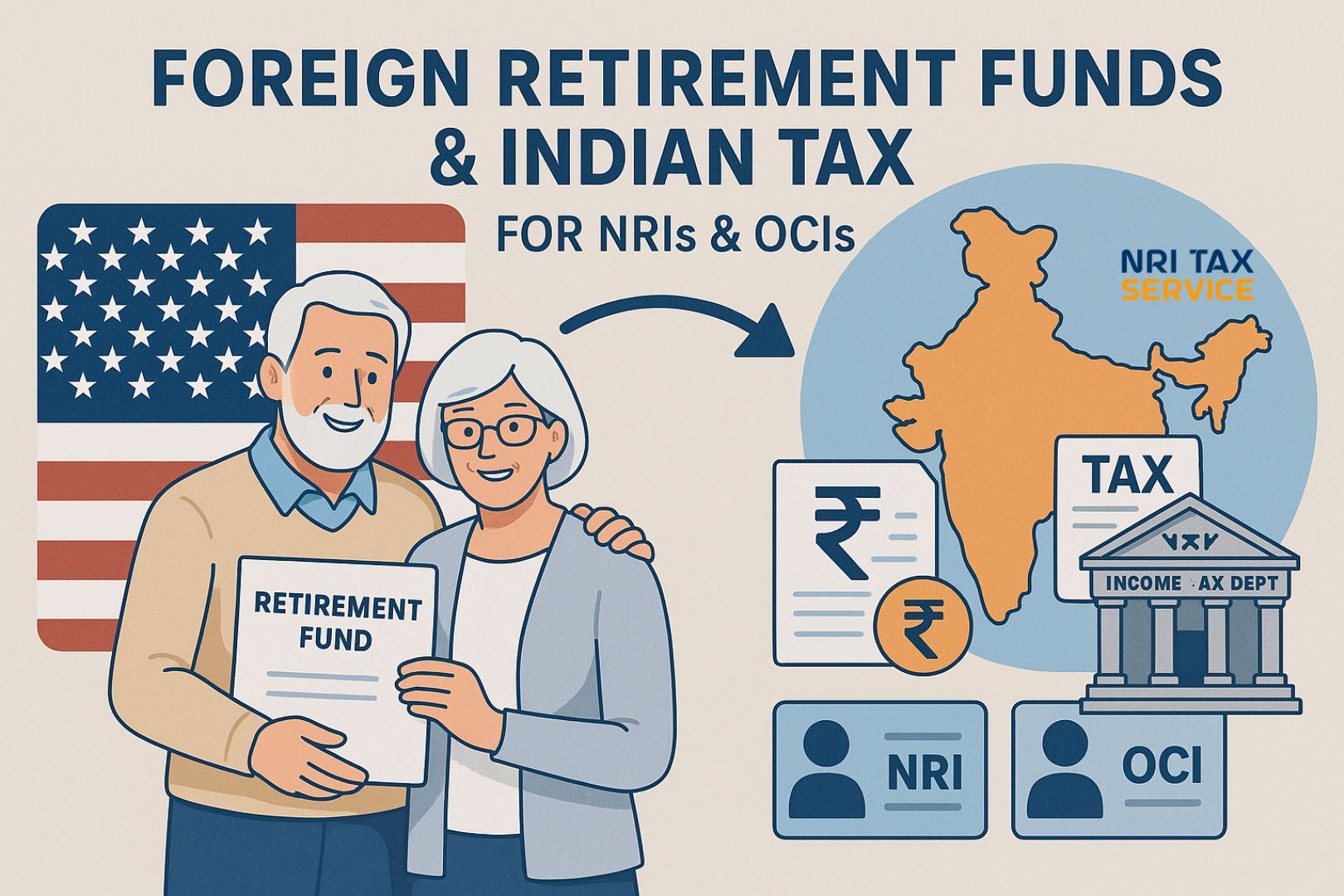

Returned NRIs and OCIs often face uncertainty regarding the taxability of foreign retirement funds in India, including accounts such as 401(k), IRA, and RRSP. Indian tax law now provides relief through Section 89A and Rule 21AAA, allowing deferral of taxation to the year of withdrawal if certain conditions are met.

You may like

1.00

Auto insurance in Fargo and car insurance in Fargo: A guide to informed decisions |

auto insurance in Fargo